Boarding Your Investment Property: Tax and Legal Rules

Thinking about turning your investment property into a boarding house? It's a smart move for many Kiwis chasing higher yields and tax perks, but navigating the tax and legal rules is crucial to avoid...

Sarah covers personal finance, tax, and KiwiSaver topics for Lifetimes NZ. She focuses on making money management straightforward and practical for everyday Kiwis.

Thinking about turning your investment property into a boarding house? It's a smart move for many Kiwis chasing higher yields and tax perks, but navigating the tax and legal rules is crucial to avoid nasty surprises from the IRD or Tenancy Tribunal.

With residential investment interest deductibility now fully restored to 100% from 1 April 2025, standard rentals are looking healthier, yet boarding houses offer unique exemptions and cash flow advantages that could supercharge your portfolio. In this guide, we'll break down everything you need to know about boarding your investment property under 2026 New Zealand rules—from High Court criteria to RTA obligations, tax treatments, and practical tips to get started right.

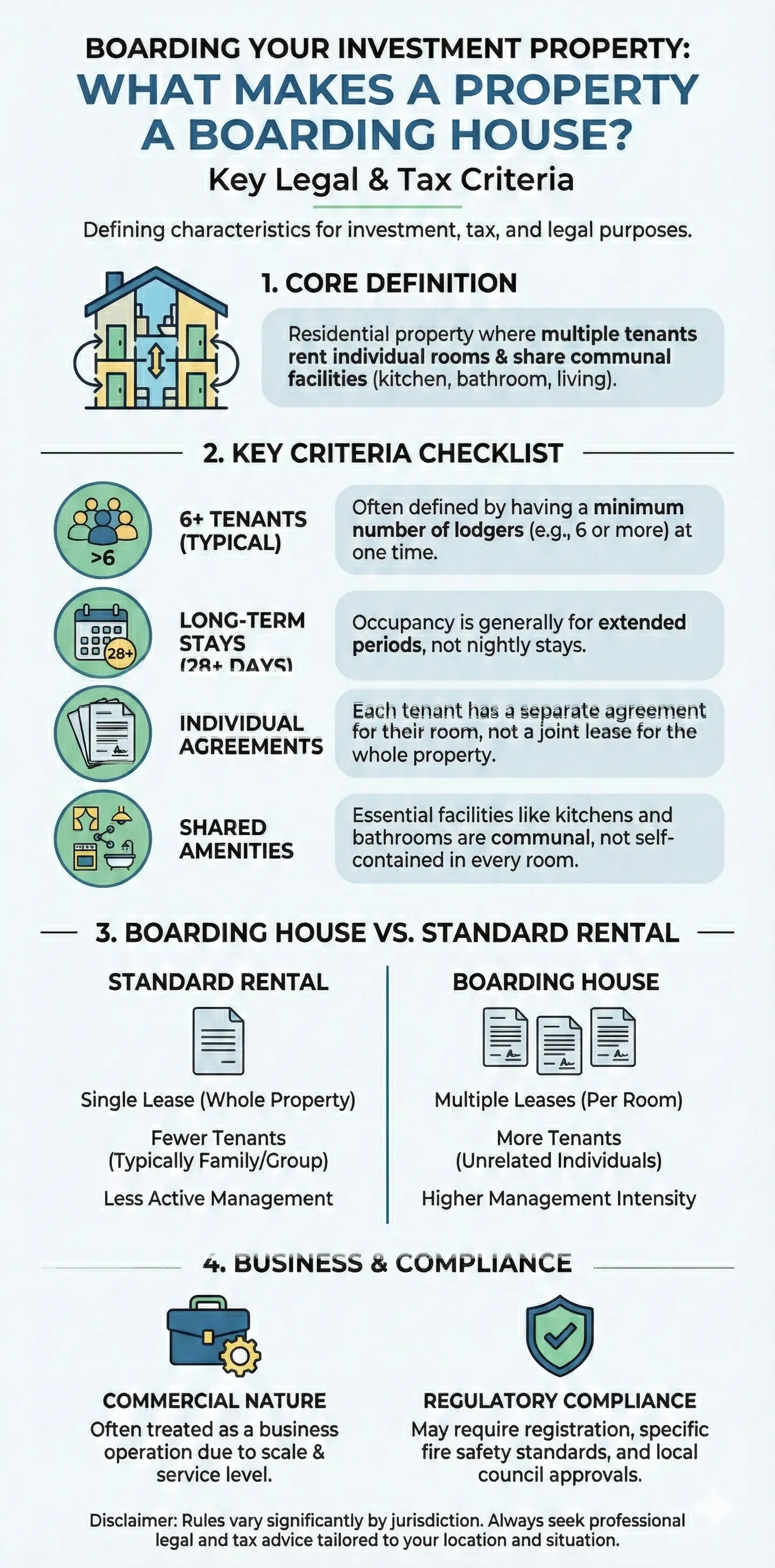

What Makes a Property a Boarding House?

Not every multi-tenant setup qualifies as a boarding house. The High Court case Karmarkar v Pandem & Ors set clear benchmarks that the IRD and courts use to classify them, exempting qualifying properties from certain residential tax restrictions.

To be deemed a boarding house, your property must tick these boxes:

- Contains one or more bedrooms plus communal facilities (like kitchens or lounges) for tenant use.

- Occupied or intended for 6 or more tenants.

- Tenancies last 28 days or longer.

- Tenants have exclusive rights to specific bedrooms via individual tenancy agreements—not collective decisions.

Pro tip: If you're short on tenants, you can't artificially qualify—intent and actual use matter. Location is gold: target areas near unis, malls, or transport hubs for steady demand from students, workers, or migrants without cars.

Boarding vs Standard Rental: Key Differences

Boarding houses fall under the Residential Tenancies Act (RTA) but with tailored rules. They must comply with Healthy Homes Standards by 1 July 2021 (first deadline), and you'll display house rules and fire evac plans prominently.

| Aspect | Standard Rental | Boarding House |

|---|---|---|

| Bond | Up to 4 weeks' rent | Up to 4 weeks' rent (same) |

| Rent Increase Notice | 60 days (fixed-term) or 28 days (periodic) | 28 days |

| Access to Facilities | Exclusive use of whole property | Guaranteed access to room, toilet, bathroom at all times |

| Termination Notice | Standard RTA grounds | 28 days general; 48 hours for unpaid rent (after 10-day notice); immediate for damage/threats |

These tweaks make management tighter but enable higher occupancy and yields—aim for 7% gross in prime spots.

Tax Rules for Boarding Your Investment Property

Boarding houses sidestep many residential rental headaches, treating them more like commercial operations for tax purposes. You're exempt from phased interest deductibility limits that hit standard rentals pre-2025.

Interest Deductibility: The Big Win

From 1 April 2025 (tax year ending 31 March 2026), all residential rentals—including boarding houses—claim 100% mortgage interest against rental income. But boarding houses were exempt from the 2021-2025 phase-out (0% to 80%), letting you load debt strategically from other properties.

Example: A $1m property with $800k mortgage at 6% interest costs $48k/year. Pre-2025, a standard rental might deduct only 80% ($38.4k), taxing the rest. Now, deduct it all—saving thousands at your marginal rate (up to 39%).

Income and Expense Calculations

Use the actual cost method: deduct expenses from gross rent to find taxable profit. For boarding income:

- Standard Weekly Cost: Up to $186/week per boarder (max 4 for this method) from 1 April 2019. Excess over this is taxable.

- Annual Housing Standard-Cost: 4% of property value (incl. improvements). E.g., $450k house = $18k threshold; income above is taxable.

- Actual Calculation: Track real income/expenses for precision—best for 6+ boarders.

Three boarders at $200/week for 39 weeks: $23.4k income. Method (a): Tax $1.638 excess. Method (b): If under $18k annual cost, zero tax.

"If run well, these properties should be cash cows—achieving at least 7% gross yield is definitely viable."

Bright-Line Test and Capital Gains

No general CGT in NZ, but bright-line rules tax residential land sales within 2 years of purchase (10 years for some pre-2024 buys—check your date). Boarding houses may qualify as business use, potentially exempting gains—consult IRD or an accountant.

GST Rules: Watch the Four-Week Trap

If stays exceed 4 weeks from the start, charge GST on 60% of domestic goods/services value immediately—not after 4 weeks. Register if turnover tops $60k/year (standard threshold).

Legal Requirements and Compliance

Beyond RTA, meet building warrants, fire regs, and Healthy Homes. Display rules/evac plans; ensure 24/7 facility access.

Setting Up Your Boarding Operation

- Assess Property: Fit-out for 6+ rooms? Communal areas?

- Individual Agreements: Exclusive bedroom rights per tenant.

- Insurance Check: Landlord policies often exclude boarding—get specialist cover.

- Resource Consents: Some councils require for high-density.

- IRD Notify: Update rental income type for correct tax treatment.

Actionable Tip: Start small—convert 4-5 rooms while testing demand via Trade Me or Facebook Marketplace.

Pros and Cons of Boarding Houses in 2026

| Pros | Cons |

|---|---|

| 7%+ gross yields | Higher management time |

| Tax exemptions/premiums | Stricter RTA compliance |

| Steady long-term tenants | Upfront fit-out costs |

| Debt-loading strategy | GST complexity |

National's 2025 reversal levels the field—no more new-build premiums or social housing hacks needed.

Practical Tips for Kiwi Investors

- Shift debt from phasing-out rentals to boarding for max deductions.

- Use KiwiSaver for deposits but factor withdrawal taxes (PIR capped at 28%).

- Track everything via Xero or FreeAgent for IRD audits.

- Join Property Investors Federation for templates and advice.

- Budget for maintenance—Healthy Homes fixes aren't cheap.

Current rates: Marginal tax up to 39%; RWT on interest to 39%. Always verify with ird.govt.nz tools.

FAQ

1. Are boarding houses still exempt from interest deductibility rules in 2026?

Yes, they were always exempt, and now all rentals get 100% from April 2025.

2. How many tenants do I need?

Minimum 6 for High Court definition.

3. Do I need to charge GST?

If over $60k turnover or 4+ week stays trigger the 60% rule.

4. What's the rent increase process?

28 days' notice; no more than once every 12 months.

5. Can I convert my existing rental?

Yes, but check consents, insurance, and refit for communal spaces.

6. How do I calculate taxable boarding income?

Choose standard cost ($186/week max 4), annual 4% property value, or actuals.

Next Steps to Board Your Property

Ready to boost cash flow? Chat with your accountant or tax advisor first—this isn't advice, just info. Check IRD's property hub, draft tenancy agreements via tenancy.govt.nz, and crunch numbers with a spreadsheet. With 100% deductibility locked in, 2026 is prime time for boarding savvy. Get professional financial advice tailored to your situation.

Related Articles

Industry Bodies and Professional Associations NZ

Whether you're launching a business, advancing your career, or navigating financial regulations, industry bodies and professional associations in New Zealand offer invaluable support. These organisati...

Emergency Benefit NZ: When You Have No Other Options

When you're struggling financially and don't qualify for other benefits, the Emergency Benefit might be your lifeline. It's a discretionary payment designed for Kiwis in genuine hardship who've exhaus...

Unpaid Internships NZ: Are They Legal?

Unpaid internships are a common pathway for students and graduates to gain work experience in New Zealand, but there's often confusion about whether they're actually legal. The short answer is: unpaid...

Estate Administration NZ: Managing Someone's Affairs After Death

Losing a loved one is one of life's toughest challenges, and stepping in to manage their estate can feel overwhelming. In New Zealand, estate administration—the process of handling someone's affairs a...