Small Business Tax Guide: What NZ Freelancers Need to Know

Freelancing in New Zealand offers the freedom to be your own boss, but it comes with the responsibility of handling your own taxes. Whether you're a graphic designer in Auckland, a consultant in Welli...

The Lifetimes NZ editorial team curates, fact-checks, and updates guides on personal finance, property, health, immigration, legal, business, and lifestyle topics relevant to Lifetimes NZ readers. Articles are produced with AI assistance and reviewed by the editorial team before publication.

Freelancing in New Zealand offers the freedom to be your own boss, but it comes with the responsibility of handling your own taxes. Whether you're a graphic designer in Auckland, a consultant in Wellington, or a tradie in Christchurch, understanding your tax obligations ensures you stay compliant with IRD and maximise your deductions.

As a sole trader or freelancer, your business income is taxed as personal income, but you've got opportunities to claim expenses and potentially save thousands. This guide breaks down everything you need to know for the 2026 tax year, from income tax rates to GST rules and top deductions.

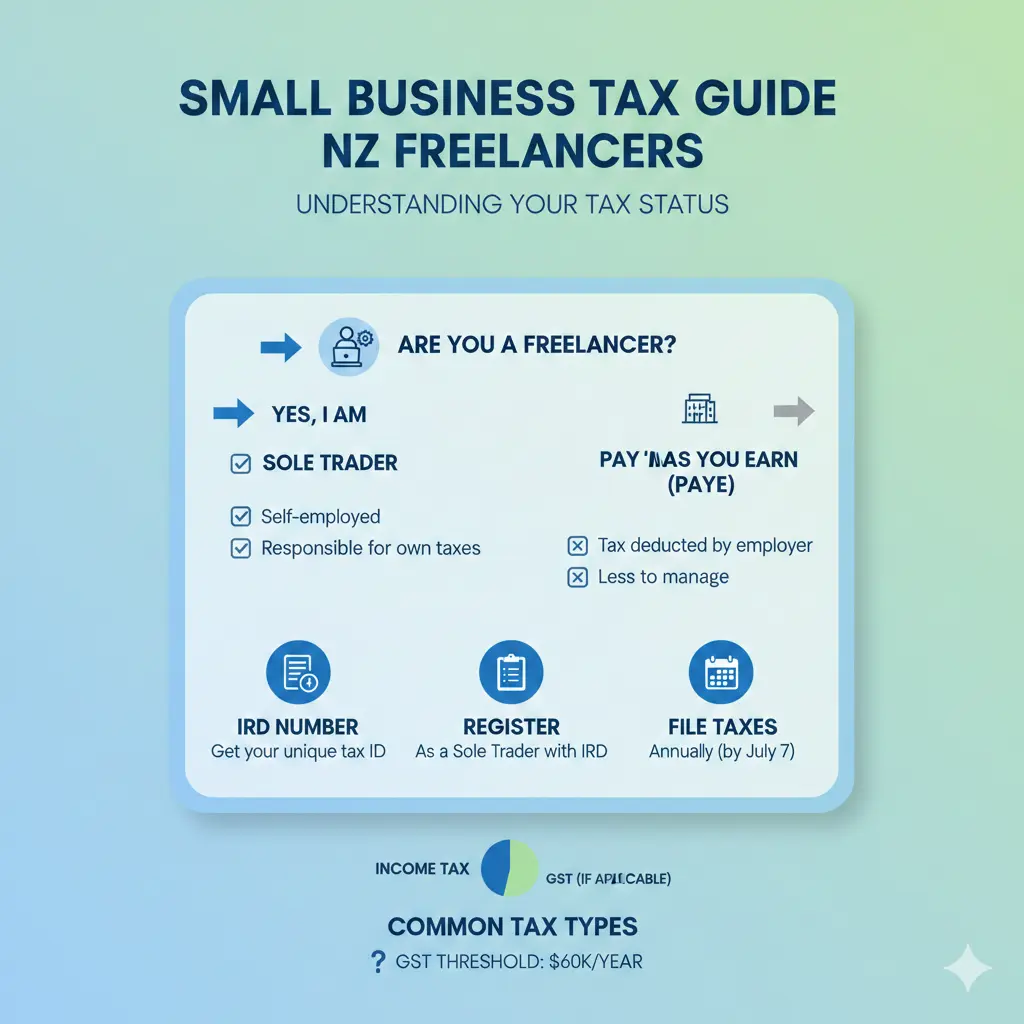

Understanding Your Tax Status as a NZ Freelancer

Most freelancers operate as sole traders, the simplest business structure in New Zealand. This means you use your own IRD number, and your business profits are taxed at personal income tax rates. No need for a separate company setup unless your turnover grows significantly.

Key responsibilities include:

- Filing an IR3 income tax return by 7 July (or later with an agent) for the year ending 31 March.

- Paying provisional tax if your residual income tax exceeds $5,000—typically in four instalments.

- Handling ACC levies based on your industry's risk level.

- Registering for GST if your turnover hits $60,000.

Pro tip: Get an IRD number if you don't have one already via ird.govt.nz. It's free and essential for freelancers.

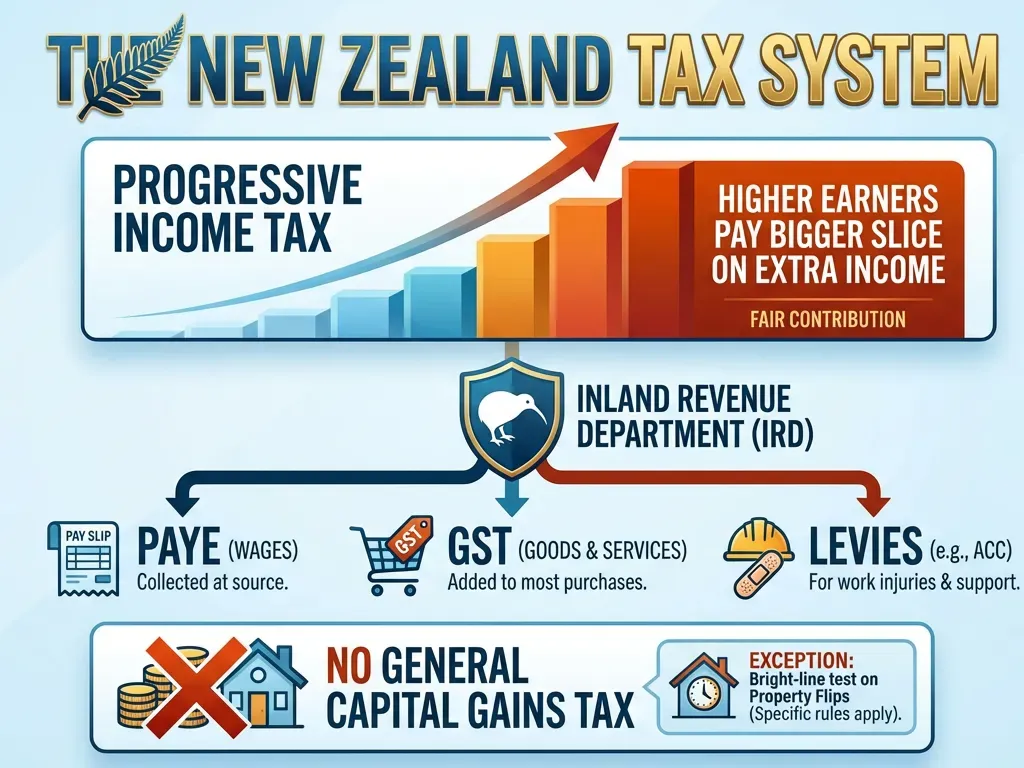

Income Tax Rates for 2026

For the 2025/26 income year (1 April 2025 to 31 March 2026), New Zealand's progressive tax rates apply to your net profit (income minus deductible expenses). Here's the breakdown:

| Income Range | Tax Rate |

|---|---|

| $0 – $15,600 | 10.5% |

| $15,601 – $53,500 | 17.5% |

| $53,501 – $78,100 | 30% |

| $78,101 – $180,000 | 33% |

| Over $180,000 | 39% |

Example: If your net profit is $60,000, your tax bill would be around $11,020 after progressive calculations—about 18.4% effective rate. Use IRD's online calculator for precision.

GST Rules for Freelancers

GST (Goods and Services Tax) is 15% in New Zealand, but as a freelancer, you're only required to register if your annual taxable supplies exceed $60,000 (including what you expect to earn).

If registered:

- Charge 15% GST on your invoices and pay it to IRD (monthly, bi-monthly, or six-monthly).

- Claim back GST on business purchases—like software, office supplies, or travel.

Not registered? You can't claim input GST, but life is simpler—no GST on quotes. Many freelancers under $60k stay unregistered to avoid admin hassle. If you're close to the threshold, track your turnover monthly.

When to Register for GST

Register voluntarily if it benefits you (e.g., lots of GST-eligible expenses). Use IRD's GST registration form online. Once registered, you're in for at least two years.

Top Tax Deductions for NZ Freelancers

Deductions are your best friend—they reduce your taxable income. Claim anything wholly and exclusively for business, with receipts.

Common claims include:

- Home office: Portion of rent, power, internet (e.g., 20% of your house if that's your workspace). Use IRD's square metre method.

- Vehicle expenses: Logbook method (track business km) or mileage rate (79c/km for 2026, confirm with IRD).

- Marketing & subscriptions: Website hosting, Google Ads, LinkedIn Premium.

- Professional fees: Accountant, lawyer, software like Xero.

- ACC levies: Fully deductible; pay via CoverPlus Extra for flexibility.

- New in 2026: 20% Investment Boost on new assets over $1,000 bought from 22 May 2025—instant depreciation kick.

Keep digital records for seven years—IRD audits are real. Apps like Xero or QuickBooks make this easy for freelancers.

Employee or Contractor Expenses

If you hire help, deduct wages, KiwiSaver contributions (minimum 3% employer match), and ACC levies. Ensure contractors are truly independent to avoid IRD reclassification.

Provisional Tax and Payments

If your tax bill tops $5,000, pay provisional tax in instalments: 6 August, 15 November, 28 February, 15 May. IRD estimates based on prior years; pay more if you're growing.

Shortfall penalties apply if underpaid, plus Use-of-Money Interest (UOMI). Pay on time to avoid this—set calendar reminders.

ACC Levies for Self-Employed Kiwis

ACC covers injuries, but self-employed pay your own levies based on earnings and industry risk (e.g., office work is low, construction high). Rates for 2026: Expect around 1.35% average, but check your category.

Options: CoverPlus (standard) or CoverPlus Extra (choose coverage level). Levies are tax-deductible.

Filing Your Taxes: Step-by-Step

- Gather records: Invoices, receipts, bank statements.

- Calculate net profit: Income minus expenses.

- File IR3: Online via myIR by 7 July 2026 for 2025/26 year.

- Pay any balance: By due date to qualify for first-year discounts if applicable.

Use an accountant for complex cases—fees are deductible and save headaches.

Common Mistakes to Avoid

- Mixing personal and business bank accounts—get a separate business one.

- Forgetting provisional tax, leading to UOMI.

- Claiming non-deductible items like home groceries or fines.

- Missing GST registration deadline—penalties start at $250.

Next Steps for Freelance Tax Success

Start by reviewing your 2025/26 finances now—set up proper tracking in Xero or similar. Chat with an IRD-registered accountant for personalised advice, especially on deductions and GST. Visit ird.govt.nz/myir to file easily, and check business.govt.nz for free webinars.

Remember, tax rules change, so this isn't personalised advice—consult a professional to avoid penalties. Stay compliant, claim what's yours, and keep more of your hard-earned cash.

Frequently Asked Questions

Sources & References

-

1

Tax basics for sole traders - Business.govt.nz — www.business.govt.nz

- 2

-

3

A beginner's guide to tax for self-employed people - Afirmo NZ — www.afirmo.com

-

4

New Zealand PAYE Tax Rates 2025 & 2026 - MoneyHub — www.moneyhub.co.nz

-

5

U.S. Expat Taxes in New Zealand: Income Tax Guide & NZ Tax Rates - Taxes for Expats — www.taxesforexpats.com

-

6

Expatriate tax - New Zealand - Grant Thornton International — www.grantthornton.global

-

7

Self-employed - Inland Revenue — www.ird.govt.nz

- 8

Related Articles

Tax Refund Secrets: How to Claim Every Dollar from the IRD This Year

Ever felt like the IRD owes you money but you're not sure how to get it back? You're not alone—many Kiwis leave hundreds of dollars on the table each year simply because they don't know the tax refund...

Best Accountant for NZ Property Investors

Owning rental properties in New Zealand can build serious wealth, but navigating the tax rules often feels like a minefield. The right accountant doesn't just file your returns—they spot deductions, s...

NZ Tax System Basics: PAYE GST and More

Ever wondered why your paycheck shrinks more than expected, or how that 15% added to your coffee bill funds our roads and hospitals? You're not alone—navigating the NZ tax system basics like PAYE, GST...

IRD Refunds and Tax Returns: How to Claim What You're Owed

If you've been paying tax in New Zealand, you might be owed money back. The Inland Revenue Department (IRD) processes thousands of refunds every year, and the good news is that for most Kiwis, claimin...